What Is Form 16? A Practical Guide for HR and Payroll Teams

Summary

This blog explains what Form 16 is and why it matters for employers and employees. It covers its structure, issuance rules, TRACES downloads, compliance requirements, and the upcoming shift to Form 130 under India's new tax framework.

Form 16, as we have known in India for decades, is officially in its final year of existence. Every tax season, employees Google 'Form 16 kya hai' or 'Form 16 kya hota hai' while trying to understand salary TDS or ITR filing or sometimes tax deductions.

In this detailed guide, we cover Form 16 meaning, its two-part structure, the TRACES download process, and more.

Most critically, we will talk about the transition to Form 130 that every HR and payroll team in India must now be acting on.

Form 16 Meaning, Purpose, and Legal Basis

What Is Form 16?

In simple terms, Form 16 means a TDS certificate issued by an employer to a salaried employee under Section 203 of the Income-tax Act, 1961. It acts as proof that tax has been deducted from salary and deposited with the Central Government.

Banks accept Form 16 as income proof for loans. Thus, employees can use it to file their Income Tax Return.

Who Issues Form 16?

Only employers who deduct TDS on salary under Section 192 are mandated to issue it.

If no TDS was deducted because the employee's income was below the basic exemption limit, you are not legally bound to issue Form 16, though many companies still provide a salary certificate for goodwill.

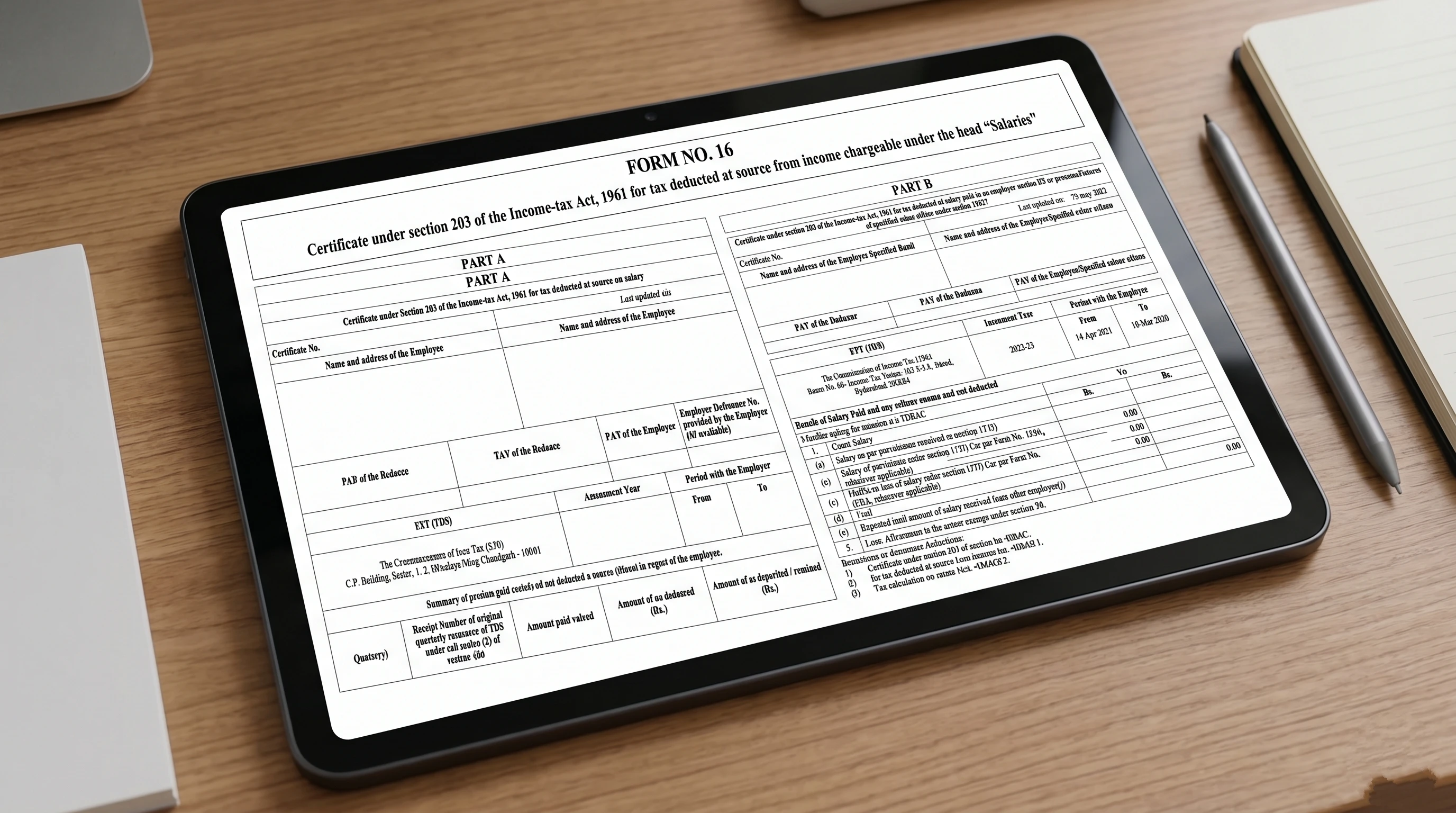

Understanding Part A and Part B of Form 16

Form 16 has two distinct parts. Mixing them up is one of the most common errors seen in payroll operations across industries.

Part A: System-Generated TDS Summary from TRACES

Part A is auto-generated by the employer from the TRACES portal (TDS Reconciliation Analysis and Correction Enabling System, at tdscpc.gov.in). It contains:

- Name, address, PAN, and TAN of the employer

- Name, address, and PAN of the employee

- Quarter-wise TDS deducted and deposited with the government

- A digital signature confirming authenticity

Part A is tamper-proof by design. Employees who worked with multiple employers during a financial year receive a separate Part A from each employer for their respective period.

Part B: Employer-Prepared Salary and Deduction Breakdown

Part B is prepared independently by the employer and functions as a detailed annexure. It covers:

- Gross salary components (basic, HRA, special allowances, bonus, perquisites)

- Exemptions allowed under Section 10 (HRA, LTA, etc.)

- Standard deduction (₹75,000 under the new tax regime for FY 2024-25; ₹50,000 under the old regime)

- Deductions under Chapter VI-A (Sections 80C, 80D, 80CCD, etc.)

- Net taxable income

- Total tax liability and TDS deducted during the year

Part B is where most errors originate. Relying on modern payroll software like Mewurk goes a long way in automating complete salary calculations alongside investment declarations and deduction tracking, which is crucial for reducing mismatches between Form 16 and Form 26AS.

A misclassified allowance, a missed investment declaration, or an incorrectly populated deduction creates a mismatch between Form 16 and the employee's Form 26AS. That mismatch is what generates tax notices.

Who Is Required to Receive Form 16?

Employees get Form 16 only if their employer deducted TDS from their salary. Being a salaried employee alone does not automatically mean you will receive Form 16.

The table below gives a quick practical breakdown of eligibility to receive Form 16.

| Category | Exemption Limit (FY 2024-25) | Form 16 Mandatory? |

|---|---|---|

| New Tax Regime employees | Income exceeds ₹3,00,000, TDS deducted | Yes |

| Old Regime employees (below 60 years) | Income exceeds ₹2,50,000, TDS deducted | Yes |

| Senior Citizens, Old Regime (60-80 years) | Income exceeds ₹3,00,000, TDS deducted | Yes |

| Super Senior Citizens (above 80 years) | Income exceeds ₹5,00,000, TDS deducted | Yes |

| Employees below exemption limit, no TDS | Not applicable | Not legally required |

HR Best Practice: Even where no TDS is deducted, many organisations issue Form 16 as standard policy. It benefits employees who require proof of income for home loans, visa applications, and tenancy agreements.

Key Form 16 Changes for FY 2024-25

The Form 16 issued for FY 2024-25 (Assessment Year 2025-26) comes with a few important updates following the Union Budget 2024 and recent CBDT notifications. It means you cannot reuse last year's template.

TDS and TCS from Other Income Sources Now Disclosed

The updated framework allows employers to co-adjust TDS and TCS from external sources such as fixed deposit interest or foreign travel expenditures directly during monthly payroll runs.

If your employees have formally declared these external liabilities, you must ensure these metrics are accurately aggregated and reflected within the updated Form 16 and Form 24Q formats.

Higher Standard Deduction Under the New Tax Regime

The standard deduction for employees opting for the new tax regime rose to ₹75,000 for FY 2024-25, compared to ₹50,000 previously. The old regime retains the ₹50,000 standard deduction. Part B of Form 16 will reflect whichever figure applies based on the employee's declared regime.

Enhanced NPS Employer Contribution Deduction

Under the new tax regime, employees can now claim a deduction of up to 14% of basic salary under Section 80CCD(2) for employer contributions to the National Pension System, which is up from 10% under the old regime.

This change appears in Part B and requires confirmation that the correct percentage is being applied per regime.

Mandatory Tax Regime Declaration in Records

Securing explicit, documented choices between the old and new tax regimes at the beginning of the financial year remains a critical internal control.

Because this selection dictates the entire exemption pipeline and structures Part B data, you should have strong collection mechanisms to ensure internal payroll ledgers mirror active employee declarations.

Using modern payroll automation systems like Mewurk is highly recommended in these contexts to collect tax regime declarations digitally and maintain accurate records throughout the financial year.

PAN-Aadhaar Linkage Alert

With statutory forms increasingly tracking identity linkage status, non-linked accounts automatically trigger higher withholding tax penalties under Section 206AA.

To mitigate the risk of incorrect tax computations and subsequent penal notices, you should run a comprehensive verification audit on employee identity linkages before final processing.

How to Download Form 16 from TRACES: Step-by-Step for Employers

Employees cannot download Form 16 from any government portal directly. Only the employer has access to TRACES for this purpose. Here is the standard process:

- Log in to the TRACES website (tdscpc.gov.in) using the employer's TAN and registered credentials.

- Navigate to the "Downloads" tab and select "Form 16."

- Select the financial year (e.g., FY 2024-25 for AY 2025-26).

- Verify employee PAN details, enter TDS receipt numbers, and confirm the total TDS amounts.

- Submit the Form 16 download request. TRACES processes the request and makes files available under the Downloads section.

- Download and password-check the Form 16 download PDF. The standard password format is the employee's PAN in lowercase followed by their date of birth in DDMMYYYY format.

- Merge Part A and Part B using the TRACES PDF converter utility before issuing to employees.

Payroll tools like Mewurk make Form 16 work much easier. They keep all employee records, payroll info, and tax declarations in one place, so generating those yearly certificates is much faster.

Critical check: Part A must carry a valid digital signature from the employer before it is issued. An unsigned Part A is not a legally valid Form 16 and will cause problems during ITR verification.

Form 16 vs Form 16A vs Form 16B: The Differences in One Table

| Form | Issued By | What It Covers | Relevant Section |

|---|---|---|---|

| Form 16 | Employer | TDS on salary income | Section 192, IT Act 1961 |

| Form 16A | Banks, companies, etc. | TDS on non-salary income (FD interest, professional fees, rent) | Various sections |

| Form 16B | Property buyer | TDS deducted on immovable property sale | Section 194IA |

Your bank issues Form 16A when TDS is deducted on your fixed deposit interest. Form 16B is relevant only in property transactions. Neither of these replaces Form 16 for salaried employees.

What Happens If Form 16 Is Delayed? Important HR Compliance Rules

The deadline to issue Form 16 is June 15 of the assessment year. For FY 2026-27, that date was June 15, 2026. Delay beyond that deadline can result in attracting a penalty of ₹100 per day under Section 272A(2)(g) of the Income Tax Act, 1961, until the certificate is issued.

If you are an employer managing hundreds or thousands of employees, delayed issuance at scale multiplies financial exposure. Therefore, complete Q4 TDS reconciliation by mid-May each year and begin Form 16 generation well ahead of the June 15 deadline.

Why Form 130 Is Replacing Form 16 and What It Means for HR Teams

The Income Tax Act, 1961 was officially repealed on April 1, 2026. The Income Tax Act, 2025, and the Income Tax Rules, 2026 are now the governing framework for all salary taxation in India.

Under this new law, Form 16 has been formally replaced by Form 130, governed under Section 395 of the Income Tax Act, 2025, read with Rule 215 of the Income Tax Rules, 2026.

What Does This Mean in Practice?

For FY 2025-26 (income earned from April 2025 to March 2026), employers will still issue Form 16 in the existing format by June 15, 2026, as usual. But for Tax Year 2026-27 (income earned from April 1, 2026 onwards), the certificate that employees will receive is Form 130, to be issued by June 15, 2027.

How Form 130 Differs from Form 16

| Feature | Form 16 (old) | Form 130 (new) |

|---|---|---|

| Governing law | Section 203, IT Act 1961 | Section 395, IT Act 2025 |

| Number of parts | Two (Part A and Part B) | Three (basic details, TDS summary, detailed annexure) |

| Period terminology | Financial Year / Assessment Year | Tax Year (single unified concept) |

| Quarterly return linked to | Form 24Q | Form 138 |

| Offline issuance | Permitted | Not valid; must be issued via TRACES |

| Deduction section numbers | Old numbering (80C, 80D, etc.) | Renumbered under the 2025 Act |

The core purpose does not change. Form 130 still certifies that TDS was deducted from an employee's salary and deposited with the government. The structure used in Form 130, however, is more detailed. The three-part format will consolidate salary breakups, exemptions, deductions, and final tax liability into a single annexure. During ITR filing, you do not need to waste time cross-referencing.

How the New Tax Reporting Structure Will Impact HR and Payroll Teams

Without any doubt, the transition to the new tax reporting structure will affect payroll workflows. Here are the immediate changes HR and payroll teams should start preparing for.

- Audit your payroll software for updated section numbers, Form 138 support, and new tax validation requirements.

- Update employee communication templates to replace FY and AY terminology with the new "Tax Year" format across HR documents.

- Collect investment declarations using new Form 124 instead of the older Form 12BB format for Tax Year 2026-27.

- Generate Form 130 only through the TRACES portal since offline versions are not legally valid under the new Rules.

Common Form 16 Errors That Trigger Tax Notices

These errors cause the most downstream damages in payroll operations because they lead to ITR mismatches and tax notices later.

- PAN mismatch: Mismatch between Form 16 and Form 26AS due to an incorrectly entered PAN in the TDS return

- Allowance misclassification: Taxable allowance treated as exempt in Part B

- Regime confusion: Wrong tax regime reflected in Part B due to outdated employee declarations

- Unverified deduction claims: 80C or 80D deductions appearing in Part B without proper investment proof on file

- Unsigned Part A: Form 16 issued without a valid signature, making the certificate non-compliant during ITR filing

Conclusion

Form 16 has powered salary tax compliance in India for over six decades. Now, in a once-in-a-generation overhaul, it is making way for Form 130 under an entirely new Income Tax Act.

Whether you are issuing Form 16 for FY 2025-26 this June or preparing your payroll system for Form 130 from Tax Year 2026-27, the principles of accuracy, timeliness, and compliance remain exactly the same.

Did you find this guide useful? If yes, please share it with fellow HR leaders, payroll managers, and finance professionals in your network. Wishing you a fully compliant, error-free year ahead. Stay informed, stay ahead!

Frequently Asked Questions (FAQs)

1. What is Form 16 and what does it mean for salaried employees in India?

Form 16 is a TDS certificate issued by employers under Section 203 of the Income Tax Act, 1961. It confirms that salary tax was deducted and deposited with the government, and it is essential for filing ITR.

2. What is the last date to issue Form 16 for FY 2025-26?

You must issue Form 16 for FY 2025-26 by June 15, 2026. If it is delayed, you will attract a penalty of ₹100 per day under Section 272A(2)(g) of the Income Tax Act, 1961.

3. Can an employee download Form 16 from TRACES on their own?

No. Only employers can access the TRACES portal to download Form 16 for salaried employees. If you are an employee, you must request it from your respective HR or payroll team.

4. What is Form 130 and how is it different from Form 16?

Form 130 replaces Form 16 under the Income Tax Act, 2025, effective from Tax Year 2026-27. It has three parts instead of two and uses the new Tax Year terminology instead of Financial Year (FY) and Assessment Year (AY). The issuance of Form 130 is limited exclusively through TRACES.

5. What should HR teams do now to prepare for Form 130?

Audit your payroll software for Income Tax Act 2025 compliance, update Form 24Q references to Form 138, replace Form 12BB with Form 124 for investment declarations, and confirm your HRMS vendor has released the necessary updates.

6. What payroll software can handle Form 16?

If your organisation deals with salary processing, TDS deductions, investment declarations, and yearly tax forms, payroll software can save you from a lot of manual work and help keep everything accurate. Mewurk is one example. It lets HR and payroll teams manage employee records, salary calculations, tax declarations, and compliance tasks all from one place.

Most Popular Post

Why Accurate Attendance and Leave Management Matters for Business Growth?

Read More →Why Accurate Attendance and Leave Management Matters for Business Growth?

How To Leverage Attendance Data For Better Workforce Management?

Read More →How To Leverage Attendance Data For Better Workforce Management?